But they would be what the government consider to be ‘Essentials’ Spitty…

I know Foxy, I was being facetious to all the folks who, every time our liberties are being curtailed or a new duplicitous law installed say “if you have done nothing wrong, you have nothing to be afraid of”.

1 Like

You don’t need a digital pound to control people’s spending.

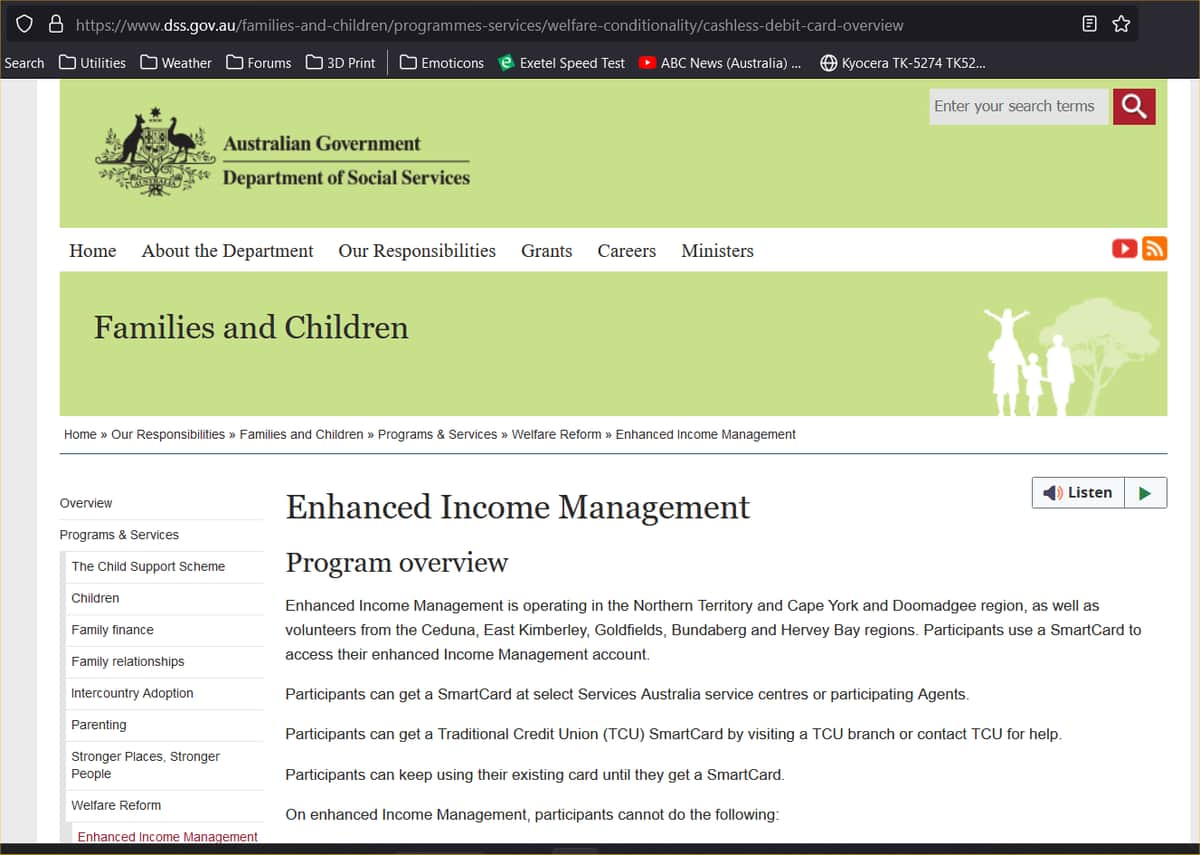

People in remote areas on social security have had their income controlled with a cashless debit card. The card couldn’t be used to purchase the following:

- buy tobacco or tobacco products

- buy pornography

- buy alcohol or homebrew kits

- gamble

- buy gift cards and cash-like products

- get cash out.

That is what will trap the popular vote, as usual, and facilitate change.

‘Page not found’ But it didn’t surprise me, Australia is fast becoming one of the most controlled countries in the world. Second only to Canada. Look how police in Melbourne persecuted and beat people for not complying with strict covid rules and refusing the vaccine. It reminded me of Nazi Germany during the war.

I checked the page is still there. No doubt your experience in Nazi Germany during the war will come in handy in the future.

With digital currency it will not only be people on benefits that will have limitations on their spending. It will be everybody.

https://www.servicesaustralia.gov.au/cashless-debit-card

Cashless Debit Card

The Cashless Debit Card (CDC) program ended on 6 March 2023.

If you had a Cashless Debit Card when the CDC program ended, and if you are eligible, you are now on enhanced Income Management.

You can keep using Cashless Debit Card to access your enhanced Income Management account until you get a SmartCard.

You can get a SmartCard at service centres or participating Agents.

1 Like

I have often watched clips of film on the BBC about life in Germany during the second world war Bruce. The burning of books, the beatings from the soldiers, and worse…You aren’t suggesting they are lying are you Bruce?

![]()

Cheers Bruce…

Apparently, the “sand dollar” was the first Central Bank Digital Currency (CBDC):

23 May 2023

The Bahamas is home not only to magnificent sandy beaches but also to the sand dollar, which when it launched in October 2020 became the world’s first Central Bank Digital Currency (CBDC). But despite being a digital currency, it most certainly should not be mistaken for cryptocurrency.

While cryptocurrencies are not managed by any central authority and their value can fluctuate – sometimes wildly – CBDCs have the same security as cash and are pegged to the value of the national currency. Over 100 countries are exploring CBDCs as central banks have come to appreciate that digital currencies are here to stay and will play a part in shaping the future of money.

However, only 11 countries so far have launched digital currencies and the results to date have been mixed. The Bahamas was a pioneer for reasons of resilience and inclusion: natural disasters such as 2019’s category five hurricane Dorian can cause massive disruption, preventing people from accessing cash from bank branches, and around a fifth of the country’s population (predominantly those on remote islands which are devoid of bank branches) do not have bank accounts in any case.

As this interesting piece on the sand dollar finds, there are still some big hurdles to overcome, notably public confusion over what a digital currency is and how safe it is, and a lack of uptake among businesses. Yet one bar owner who does accept sand dollars was enthusiastic because purchases made using the digital currency do not incur any fees, unlike the charges made for credit card transactions.

Who would have guessed … ![]()

That’s how they will sneak it in. Offer some kind of financial benefit, then when everybody is hooked, drop it, or even place a charge on it’s use…Those who control the money, control the world and everyone in it…

It won’t cost the bar tender anything too if we all used cash.

I agree that the control of money enables the control of so much more. Which is why the Americans are worried about trends by other countries to move away from the US dollar for trading. For me, the dollar has been the currency of international trade for too long.

But I cannot agree with your point about cash. Any small retailer knows that they pay for using cash. The banks charge businesses for banking with them. They charge for providing change. They charge for cashing in at the end of the day or week. Cash comes with costs and these can add up to being even higher than card / phone-pay transaction costs.

And that’s before considering the risks that cash brings.

Yes Strath, of course, I never thought of the associated costs of using cash. However, by introducing payment by card or phone we added several more ways in which the bad guys can steal your nest egg from right under your nose, and you didn’t ever know it was gone until hours later when you receive your statement or your card gets declined. At least with cash some geyser with a stocking over their head has to physically take it from you if you were careless.

Also when you pay with a card or phone you leave a trail that the authorities can follow, they like to keep tabs on where your money is coming from and where it’s going. Call me paranoid but, with cash the transaction ended the moment you hand over your money and leave the establishment…No comebacks or card cloning! After all, cash has been the prefered method of payment for thousands of years…

I remember the days before the majority of people had bank accounts, when the majority of people got paid with little envelopes containing cash with their payslips (and if you lost your pay packet or someone nicked it, there was no way of tracing them or getting your money back)

Back in those days, I used to be one of the cashiers who made up the bundles of cash in the bank. The company would send a trusted employee to the bank to collect the cash, then it would be taken back to their office to be made up into those individual packets of wages.

There was so many stages in those transactions which were opportunities for villains wearing masks to bonk someone over the head and nick the cash - and they used to.

That is why companies started paying security companies to ferry all these bundles of cash to and from the bank, which all added to their costs.

And, of course, the Banks had to pay security costs to ferry all this cash around too, which was passed on to the business customers via cash handling fees for all the notes and coin they withdrew or paid in.

Then, of course, the employees would spend the cash at the shops, which meant the shopkeepers had to ferry the cash back to the bank, incurring risk and cash handling fees.

Even back in the 1970s/80s, businesses were being charged cash handling fees based on the amount of notes and coins they paid in or withdrew and for companies employing large numbers of weekly paid staff, the cash handling fees and security costs of cash runs were costing them a lot of money. It was the risk and costs of cash handling which drove the change in the way wages were paid, which in turn drove forward the change to the way we paid for things.

My recollection of those days is that it was not the government wanting to “control the money” which drove the change away from cash payments to bank payments - it was the businesses and employers and banks who drove it forward, to reduce the risks and costs of cash handling.

I think Central Bank Digital Currencies are the next step along the same route.

I envisage they will not totally replace Cash in the near future nor will it replace our current banking services but it will be used alongside Cash and Bank Accounts - Just in the same way as switching from Cash Wages and Cash Spending to using Bank Accounts and Payment Cards did not immediately replace Cash - it’s been around 50 years since most large companies stopped paying their workers in Cash and most workers have had bank accounts but Cash hasn’t disappeared from Society yet.

I don’t envisage a U.K. Central Bank Digital Currency being the only payment option during my lifetime - though I think it will be introduced as a useful additional option.

1 Like

I can see the benefits that business and banks will enjoy from going digital Boot, and I have no doubt the world will move forward into a totally cash free society as the young inherit the earth and will have never known life without a phone or a bank account. But in a quest to make banking and business easier, It makes me wonder if the customer is being considered in all of this modernisation, where the customers only sight of their hard earned money are figures on their phone which are being remotely manipulated (direct debits etc) by companies and banks who are meant to serve us, and not the other way round…

If you think the Banks are “meant to serve us” then I’m afraid you are living in the past, back in the days when Bank Customers paid Banks to provide banking services.

The day when one Bank scrapped transactional bank charges on personal accounts, if they remained in credit, was the day which started the trend of Banks stopping putting the customers first and the day they started to look at different ways to make profits to offset the cost of providing general banking services for free.

I can clearly remember that day, in the 1980s, because it changed everything for Bank Staff. I can remember how it impacted banking services and how it forced bank staff from being “service providers” and “clerical staff” to becoming “salespeople” with “sales targets” for ancillary services to make up for the income lost when Banks were pushed into scrapping the traditional Bank Charges for personal accounts, based on account activity.

I am the past Boot…

Looking back I loved the past, the music was better, people used to meet in pubs or snooker halls, and kids played in the streets. There were no phones or internet, the telly closed down at 10:00 pm and there were very few cars. Mars bars were sixpence and stayed at that price for years. And banks were somewhere you were encouraged to save for the future…

Now the world is just sh*te!

1 Like

You are absolutely correct - the retail arms of the traditional banks are all about cross-selling you other products. But forty years on from the change in banking that you describe it looks like another big change is underway. This is the push by the big tech companies to get into payments with services like Apple Pay. This is on top of the purely online banks such as Wise or Revolut. I would be surprised if some banks simply give up on banking for individuals, and cash goes the way of cheques.